Money you can actually see.

One app. One view. Bundle multiple cards.

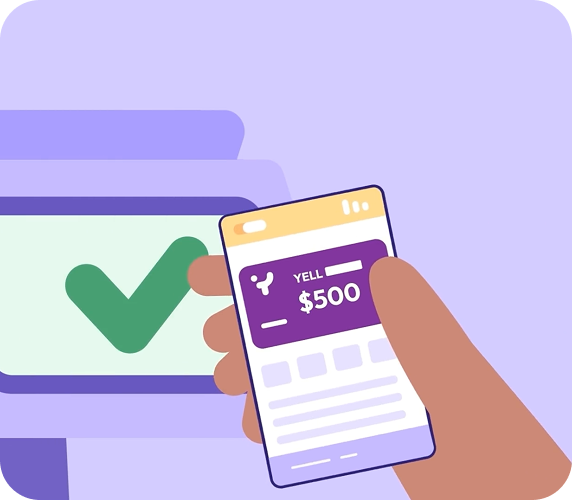

Download YELL to know what’s safe to spend, bundle for bills, and send money instantly to your YELL friends. Take control of your finances today.

More than 56,000

downloads to date

You’re the richest you’ve ever been, but why do you feel broke?

You have money, but it doesn’t feel like it. It’s spread across apps and accounts, so small charges slip through, subscriptions stack up, and you lose track of what you’ve really spent.

It shouldn’t be this hard to pay, get paid, and stay in control. YELL pulls it all back together, and lets you run your life on your own terms.

See all your money at once.

Link every account, then bundle what you need onto one secure YELL debit card. From there, spend any balance instantly.

Money that matches your lifestyle.

Add your virtual YELL card to Apple Pay or Google Pay and spend anywhere with total confidence – your money stays protected every step of the way.

Plan for life’s bigger purchases.

Whether it’s rent week, new tires, or a weekend getaway, YELL helps you set aside the amount you need for surprise bills or planned expenses.

Track those “treat

yourself” moments.

See exactly where your money goes into one dashboard. Track side income, separate it from personal spending, and download monthly statements in seconds.

Move money instantly with YELL-to-YELL.

Receive money from loved ones effortlessly, YELL-to-YELL transactions are free and instant. Sync contacts to send or request funds, add notes to keep things clear.

YELL is partnering with

Bank-level

security, built In.

Your money is always kept securely in your dedicated and FDIC* insured bank account with our partners at Bangor Savings Bank. YELL is a backed by a no-fee FDIC* insured bank account and equipped with a debit card.